As the calendar turns to the second full week of January 2026, investors, policymakers, and industry analysts are bracing for a deluge of high-impact economic data. The week of January 11, 2026, is set to provide the clearest picture yet of the U.S. economy’s trajectory as it navigates the transition into the new year. With reports ranging from inflation benchmarks to the health of the housing and manufacturing sectors, the upcoming data releases will be instrumental in shaping expectations for Federal Reserve interest rate policy and broader market sentiment.

The primary focus of market participants remains the December Consumer Price Index (CPI), alongside critical updates on retail sales and the housing market. As the Federal Reserve continues to monitor persistent inflationary pressures, the data points arriving this week will offer a granular look at whether price stability is within reach or if the "last mile" of disinflation remains as challenging as ever.

Chronology: The Week Ahead

Monday, January 12th

The week begins with a quiet start, as no major federal economic releases are scheduled. This brief lull provides market participants time to position their portfolios ahead of the high-volatility events scheduled for Tuesday through Friday.

Tuesday, January 13th

Tuesday marks the beginning of the heavy lifting. The day kicks off at 6:00 AM ET with the NFIB Small Business Optimism Index for December, offering a pulse check on the sentiment of main-street entrepreneurs facing rising operational costs and uncertain demand.

At 8:30 AM ET, the Bureau of Labor Statistics (BLS) will publish the December Consumer Price Index (CPI). Consensus estimates suggest a 0.3% increase for both the headline and core CPI, with year-over-year figures projected to hold at 2.7%. Any deviation from these expectations could trigger significant volatility in both equity and fixed-income markets.

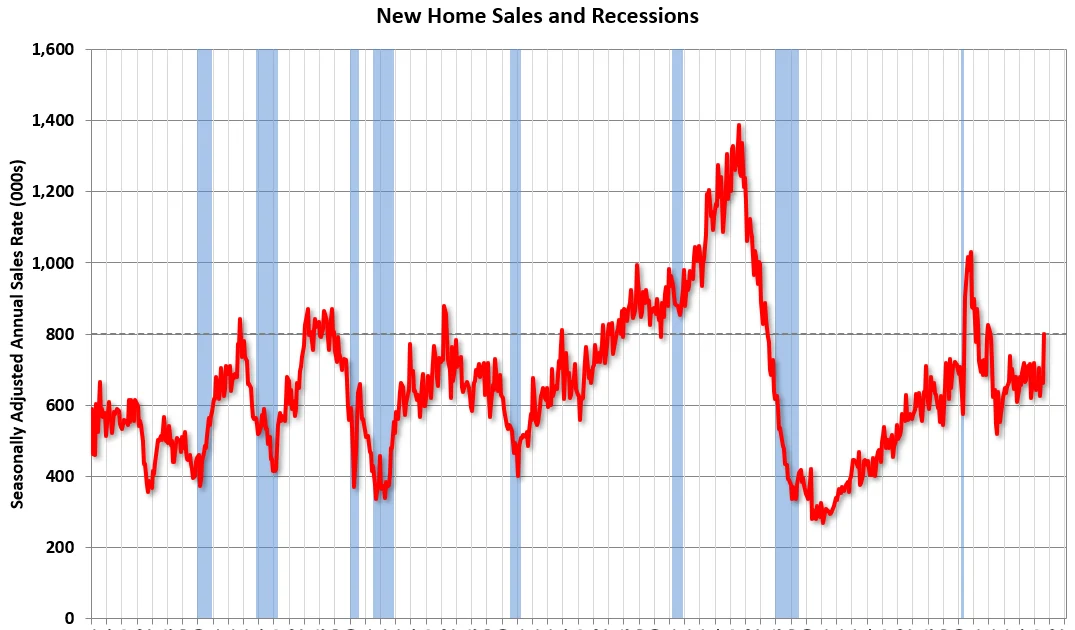

Finally, at 10:00 AM ET, the Census Bureau is slated to release the New Home Sales data for September and October. This delayed reporting schedule will be closely scrutinized to determine if high interest rates continue to suppress builder activity, with market consensus looking for a seasonally adjusted annual rate (SAAR) of 714,000 for October.

Wednesday, January 14th

Mid-week brings a concentration of retail and inflation-related data. The Mortgage Bankers Association (MBA) will release its Mortgage Purchase Applications Index at 7:00 AM ET, providing a two-week look at borrower demand in an environment of fluctuating borrowing costs.

At 8:30 AM ET, the BLS will report on the Producer Price Index (PPI) for December. With a consensus expectation of a 0.3% rise in headline PPI and a 0.2% increase in core PPI, analysts will be looking for evidence of pipeline price pressures. Simultaneously, the November Retail Sales report will be released. Analysts are currently forecasting a 0.4% increase, which would indicate resilient consumer spending despite the holiday season’s economic pressures.

The day concludes at 2:00 PM ET with the release of the Federal Reserve Beige Book. This qualitative report, which synthesizes anecdotal evidence from the 12 Federal Reserve Districts, will be vital for understanding how businesses are responding to current economic conditions on the ground.

Thursday, January 15th

Manufacturing and labor market indicators take center stage on Thursday. The weekly initial unemployment claims report will be released at 8:30 AM ET, with consensus holding steady at 208,000 claims.

Simultaneously, the regional manufacturing pulse will be measured through the New York Fed Empire State Manufacturing Survey and the Philly Fed Manufacturing Survey. The former is expected to show a slight improvement, moving to 1.0 from -3.9, while the latter is projected to recover to -5.0 from -10.2, signaling a potential stabilization in the industrial heartland.

Friday, January 16th

The week concludes with a focus on industrial output and homebuilder sentiment. At 9:15 AM ET, the Federal Reserve will release Industrial Production and Capacity Utilization data for December. Expectations point to a 0.2% increase in production, with capacity utilization remaining stable at 76.0%.

The week wraps up at 10:00 AM ET with the NAHB homebuilder survey for January. With a consensus forecast of 40—a marginal increase from 39—the index remains well below the critical 50-point threshold, underscoring the continued skepticism among builders regarding current sales conditions.

Supporting Data: Analyzing the Trends

The economic landscape heading into mid-January 2026 is defined by a delicate balance between cooling inflation and stable labor demand.

Inflationary Pressures

The CPI and PPI data are the linchpins of the week. If CPI prints higher than the 2.7% year-over-year expectation, it could dampen hopes for early rate cuts by the Federal Reserve. Conversely, a cooling PPI would suggest that the cost-push pressures on businesses are finally beginning to subside, providing a favorable backdrop for future disinflation.

The Housing Market Quandary

The housing sector continues to operate under the weight of elevated mortgage rates. While the New Home Sales data for September and October provides a historical look, it remains essential for understanding the long-term trend of housing supply. The NAHB builder survey remains the most forward-looking indicator in this space; a reading below 50 indicates that sentiment remains pessimistic, largely driven by high financing costs and labor shortages that prevent a meaningful increase in new housing inventory.

Retail Resilience

The retail sector has been the engine of the U.S. economy, consistently defying expectations of a slowdown. The November retail sales report will be a litmus test for whether consumers have finally begun to retrench. A 0.4% increase would be a positive indicator of ongoing spending power, yet it also keeps the risk of demand-pull inflation alive, a factor the Federal Reserve must weigh carefully.

Official Responses and Federal Reserve Context

The Federal Reserve Beige Book on Wednesday afternoon is perhaps the most significant "soft data" release of the week. While the CPI and retail sales numbers provide hard numerical data, the Beige Book offers the Federal Reserve’s perspective on the qualitative reality of the economy. It captures the nuances of labor shortages, supply chain bottlenecks, and wage growth that statistics alone often miss.

Market participants will be looking for clues in the Beige Book regarding how regional banks view the risk of a recession versus a "soft landing." If the district reports highlight a softening in the labor market or a pullback in consumer discretionary spending, it could signal that the Federal Reserve’s restrictive monetary policy is finally having the intended effect.

Implications for the Future

The implications of this week’s data are far-reaching. For investors, the focus is on the "pivot." If the combined reports on CPI, retail sales, and industrial production suggest an economy that is growing moderately without overheating, the equity markets may react favorably, as it supports the narrative of a soft landing.

However, if the data suggests that inflation is becoming entrenched or that the manufacturing sector is sliding into a deeper contraction, we could see a repricing of risk assets. The Federal Reserve has maintained a data-dependent stance, and this week serves as a critical checkpoint.

Key Takeaways for Market Observers:

- Interest Rate Policy: The CPI and PPI reports are the primary indicators for the Fed’s next move. If inflation remains sticky, the "higher for longer" narrative will gain momentum.

- Manufacturing Health: The regional surveys (Empire State and Philly Fed) alongside the national Industrial Production index will indicate whether the U.S. manufacturing sector is bottoming out or if global headwinds are beginning to drag down domestic output.

- Consumer Strength: Retail sales remain the bedrock of the GDP. A surprise to the downside would suggest that the high-interest-rate environment is finally eroding household savings and disposable income.

In conclusion, the week of January 11, 2026, is a high-stakes environment for all market stakeholders. With the Federal Reserve carefully monitoring these metrics to calibrate their path forward, the incoming data will not only define the immediate market reaction but also set the tone for the entire first quarter of 2026. Analysts, investors, and policymakers alike will be watching closely as the week unfolds, looking for the signals that will ultimately determine the direction of the U.S. economy.