The landscape of American financial technology is undergoing a profound transformation. According to the latest data from Tracxn, US fintech funding reached $5.1 billion in the first quarter of 2026—a striking 47% increase compared to the same period in 2025. While this headline figure suggests a robust recovery, a deeper analysis reveals a complex, multi-layered reality. The market is not merely rebounding; it is fundamentally reweighting where capital is allocated, favoring nascent innovations over legacy disruption models.

As the industry navigates the interplay between historical successes and speculative future technologies, the return of unicorns and the cautious reopening of the IPO window signal a shift in investor sentiment. The era of "growth at all costs" has been replaced by a rigorous, selective discipline, where only those startups capable of demonstrating structural scalability are securing the capital necessary to survive the current economic climate.

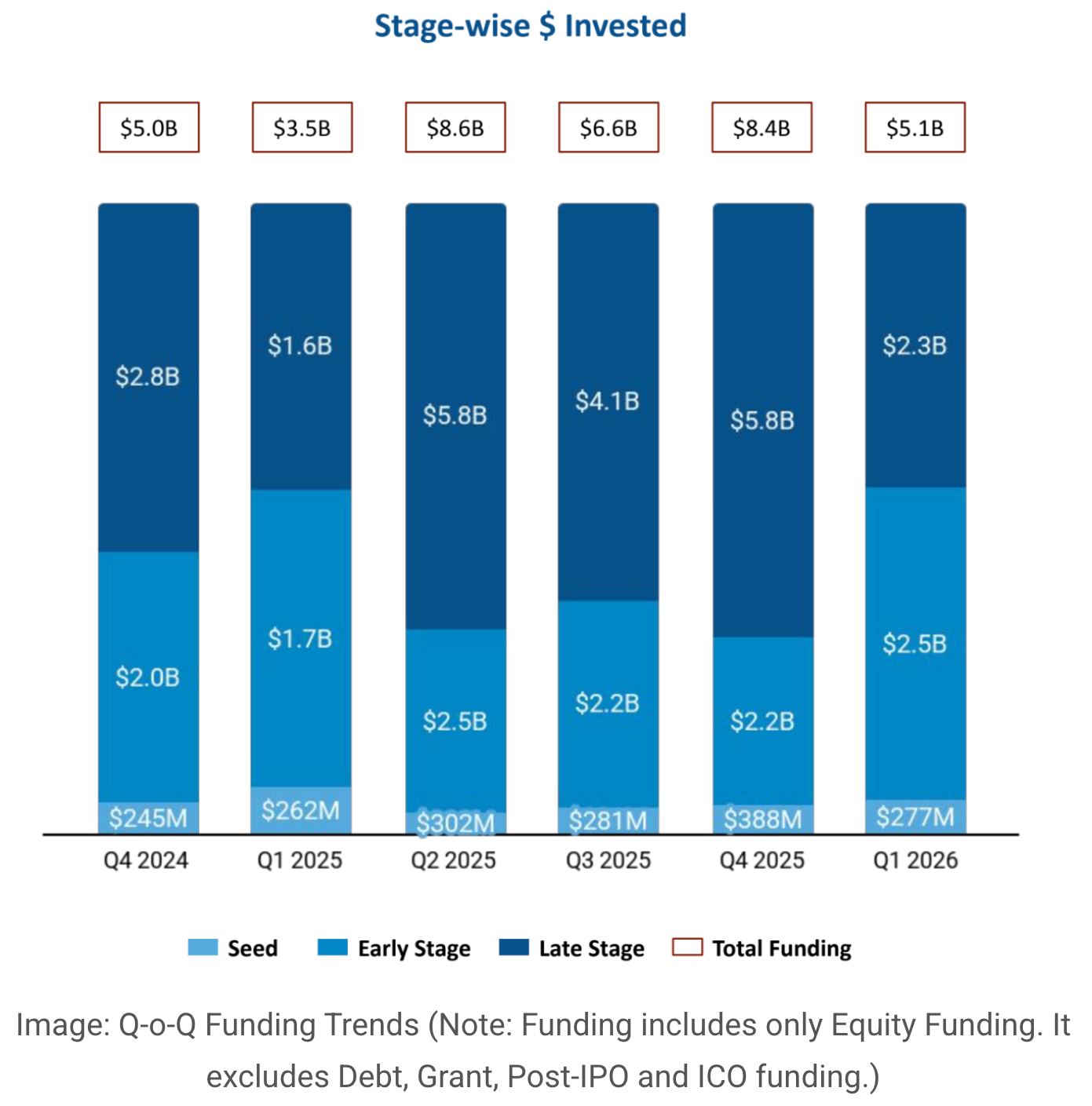

The Q1 2026 Backdrop: A Selective Market

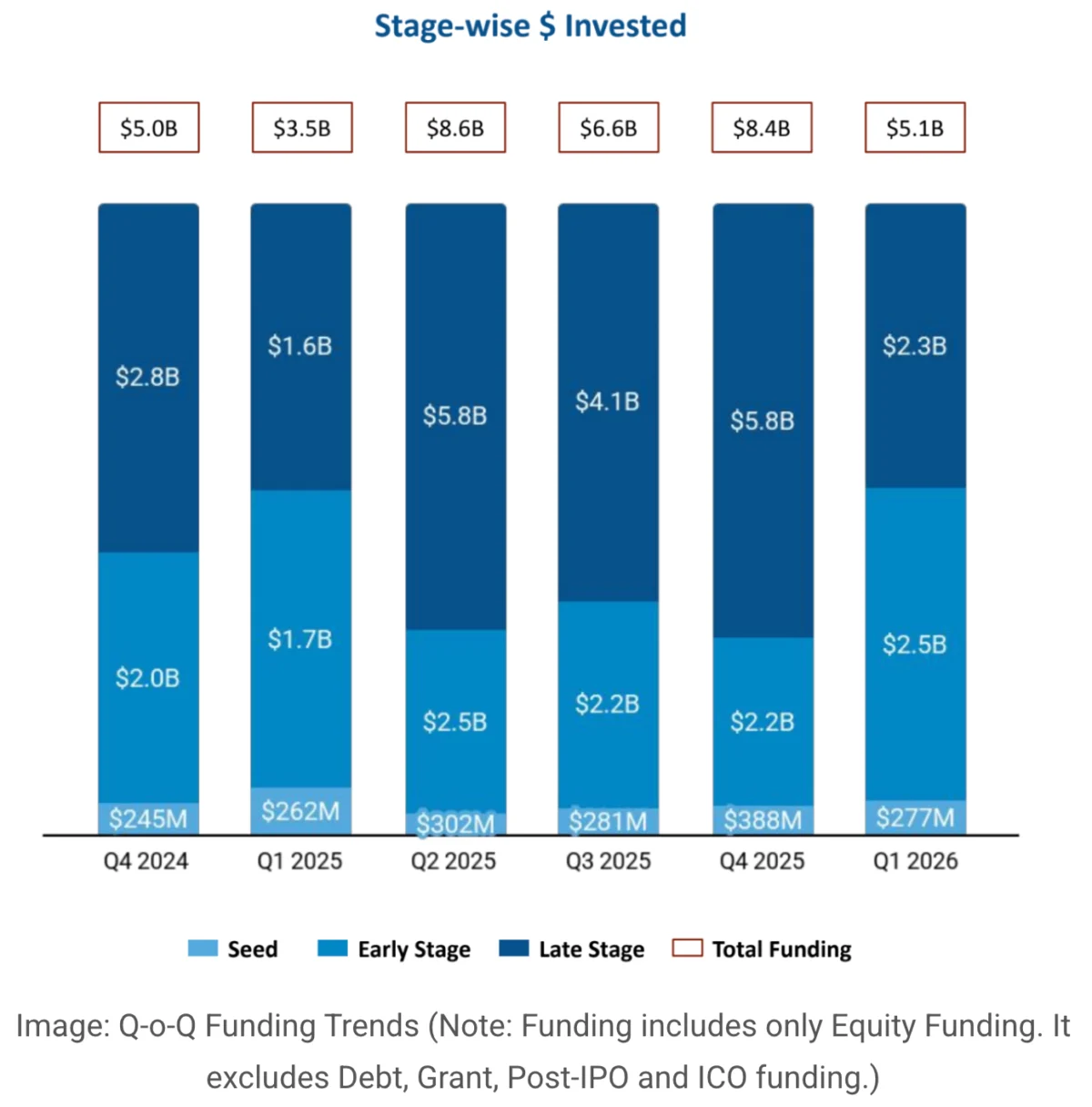

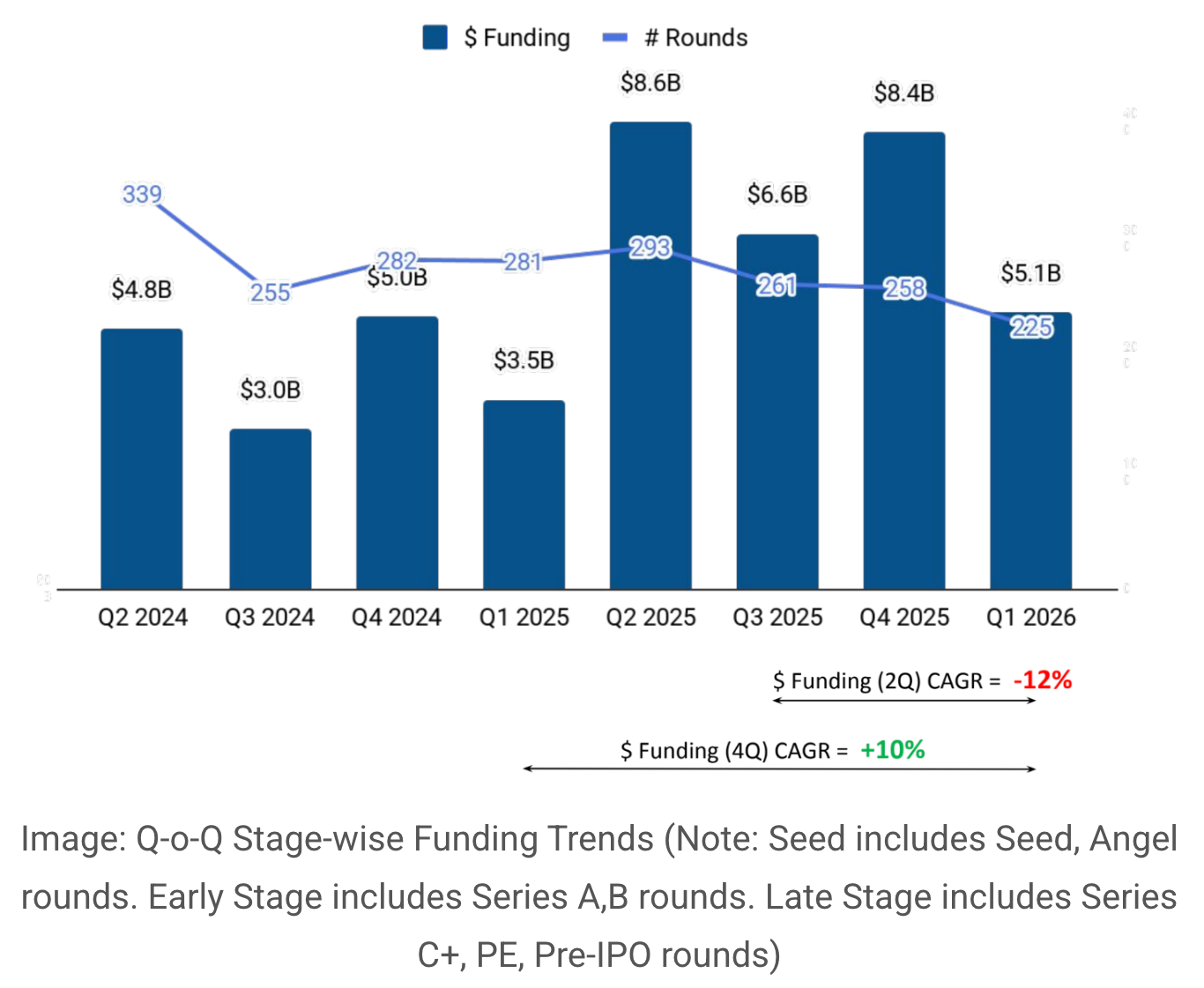

To understand the current state of fintech, one must look beyond the 47% year-over-year (YoY) growth. While the sector raised $5.1 billion, this figure represents a 39% contraction quarter-over-quarter (QoQ). This volatility is not indicative of a failing sector, but rather a reflection of a market finding a new equilibrium.

The Divergence of Capital

The Q1 data highlights a significant "conviction gap." Investors are exhibiting a renewed enthusiasm for early-stage ventures—the "hypothesis" phase of fintech—while remaining notably hesitant regarding late-stage commitments. This suggests that while venture capitalists are eager to fund the next generation of financial infrastructure, they are skeptical about the profitability and exit potential of companies that have already reached maturity but failed to achieve sustainable margins.

This environment has forced founders to pivot from expansionary tactics to efficiency-led strategies. Companies that were once valued on user acquisition numbers are now being judged by their unit economics and their ability to integrate AI into their core operations. The market is currently operating in a state of "strategic patience," where the capital is available, but the threshold for deployment has never been higher.

Chronology of the Fintech Resurgence

The path to this $5.1 billion quarter was not linear. The previous 18 months were characterized by a prolonged "fintech winter," marked by down-rounds, layoffs, and a dearth of exit opportunities.

- Q1 2025: The sector hit a valuation floor. Investors pivoted toward internal efficiency, and funding was largely confined to bridge rounds for existing portfolio companies.

- Q3 2025: Initial signs of a thaw emerged as AI-integrated financial platforms began to outperform traditional SaaS fintechs.

- Q4 2025: The IPO window began to crack open with a series of minor, but successful, public listings, signaling to the private markets that an exit path was again viable.

- Q1 2026: The current surge. The capital influx represents a transition from "survival mode" to "re-investment mode," with a specific focus on structural infrastructure rather than consumer-facing apps.

Supporting Data: The Anatomy of Investment

The data provided by Tracxn illuminates a shift in investor priorities. While consumer banking and payment processing saw moderate interest, the surge in capital is heavily concentrated in B2B infrastructure and automated financial management tools.

Key Performance Indicators (KPIs) for Q1 2026:

- Early-Stage Surge: Seed and Series A rounds accounted for nearly 55% of the total volume, indicating a strong pipeline of new ideas.

- Unicorn Re-emergence: After a drought, three new fintech unicorns were minted in Q1, signaling that the "private market premium" is returning for high-growth potential firms.

- The IPO Cautious Climate: While IPO activity is up, the average valuation at listing remains conservative. Investors are demanding proven profitability over the speculative projections that defined the 2021-2022 bull market.

The Rise of Parallel Web Systems: AI as the Primary User

The most significant trend defining this quarter is the shift toward "Parallel Web Systems." Unlike the fintech wave of the early 2020s, which focused on human-centric interfaces, current capital is flowing toward systems designed for AI as the primary user.

In this paradigm, financial software is no longer being built just to help a human accountant or a consumer manage money. It is being built to interface with Large Language Models (LLMs) and autonomous agents. These systems require high-fidelity, machine-readable data, low-latency API architectures, and robust security protocols that account for automated decision-making.

Investors are betting that the next "Trillion Dollar Fintech" will not be an app that replaces a bank, but an infrastructure layer that allows autonomous agents to execute complex financial transactions, settlements, and compliance checks without human intervention.

Official Responses and Industry Perspectives

Leading voices in the venture capital space have characterized this period as the "Great Recalibration."

"We aren’t seeing a lack of capital," says Sarah Jenkins, a senior partner at a leading fintech-focused VC firm. "We are seeing a lack of patience for models that don’t fit into the new, AI-driven financial stack. The companies that are getting funded today are those that have stopped trying to compete with incumbent banks and started trying to rebuild the pipes that banks run on."

Conversely, some market analysts express caution. The reliance on AI integration creates a new set of risks, particularly concerning systemic bias in automated lending and the potential for "algorithmic cascading failures." Regulators have begun to signal that the next wave of fintech oversight will focus heavily on the explainability of these AI-driven systems.

Implications for the Future

The implications of this $5.1 billion funding surge are twofold:

1. The Death of the "Generalist" Fintech

The market is effectively ending the era of the "all-in-one" financial app. As capital flows toward specialized, AI-native infrastructure, generalist platforms that lack a unique, defensible data moat are finding it increasingly difficult to raise follow-on funding.

2. A Shift in the IPO Narrative

The reopening of the IPO window does not signal a return to the reckless valuations of the past. Instead, the current IPO climate rewards companies with predictable, subscription-based revenue models and clear paths to regulatory compliance. The market is maturing, and the bar for public entry is being set by the performance of the latest crop of fintech companies that have survived the consolidation period.

Conclusion: Navigating the New Frontier

The Q1 2026 funding landscape is a testament to the resilience of the fintech sector. By moving away from the "growth at all costs" mentality and toward a model that prioritizes technological integration and fundamental efficiency, the industry is setting the stage for a more sustainable, albeit more competitive, future.

As we look toward the remainder of 2026, the focus will likely remain on the "Parallel Web"—the transition of financial systems from human-operated interfaces to machine-optimized protocols. For startups, the directive is clear: prove that your technology can function not just for the user of today, but for the autonomous agents of tomorrow. The capital is waiting, but the mandate for excellence has never been more stringent.