The race to dominate the artificial intelligence era has moved beyond mere model training. While the initial phase of the "AI wars" focused on foundational LLMs and compute capacity, the frontline has shifted to the application layer. Today, the three primary hyperscalers—Google, Amazon (AWS), and Microsoft—are aggressively courting AI agent startups to cement their influence over the next generation of software.

New partnership data from CB Insights reveals a clear, strategic divergence. The market is no longer a monolithic competition; instead, it is fracturing into specialized territories. Google is securing its future in the developer ecosystem, Amazon is leveraging its infrastructure dominance to own the customer service vertical, and Microsoft is entrenching itself as the undisputed sovereign of regulated enterprise industries.

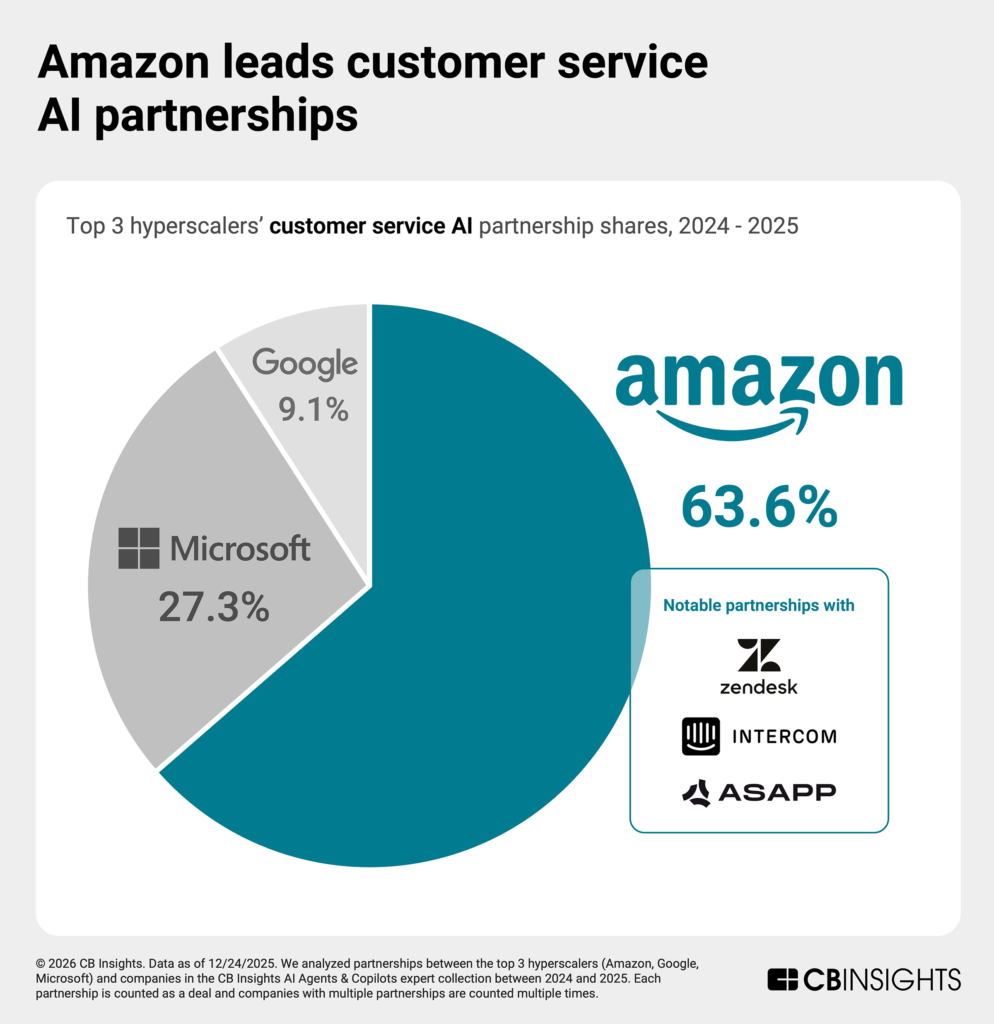

Main Facts: The Strategic Split

The landscape of AI agent partnerships is currently defined by 95 key deals signed over the last 24 months. These partnerships are not merely coincidental; they reflect a calculated land grab.

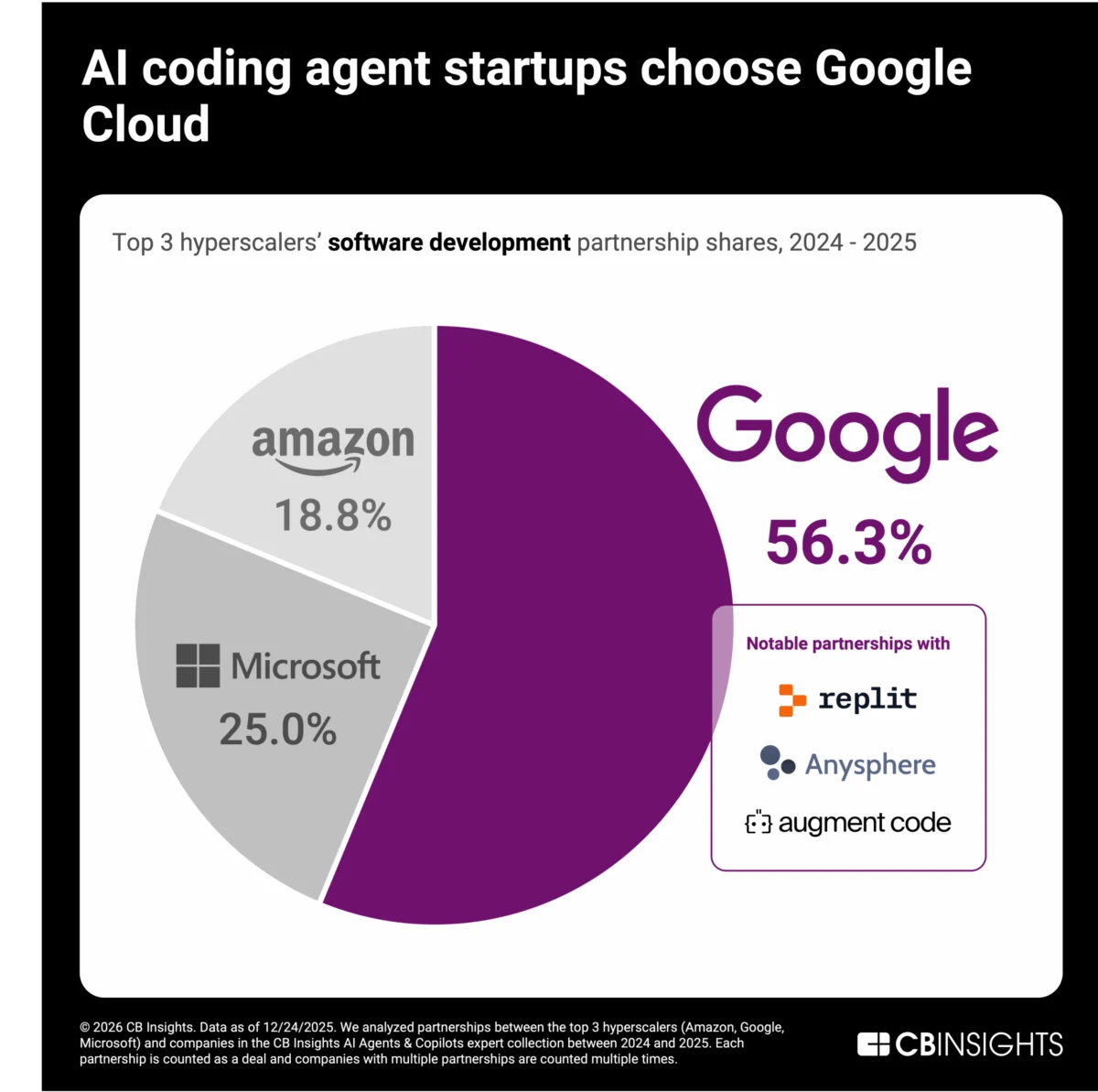

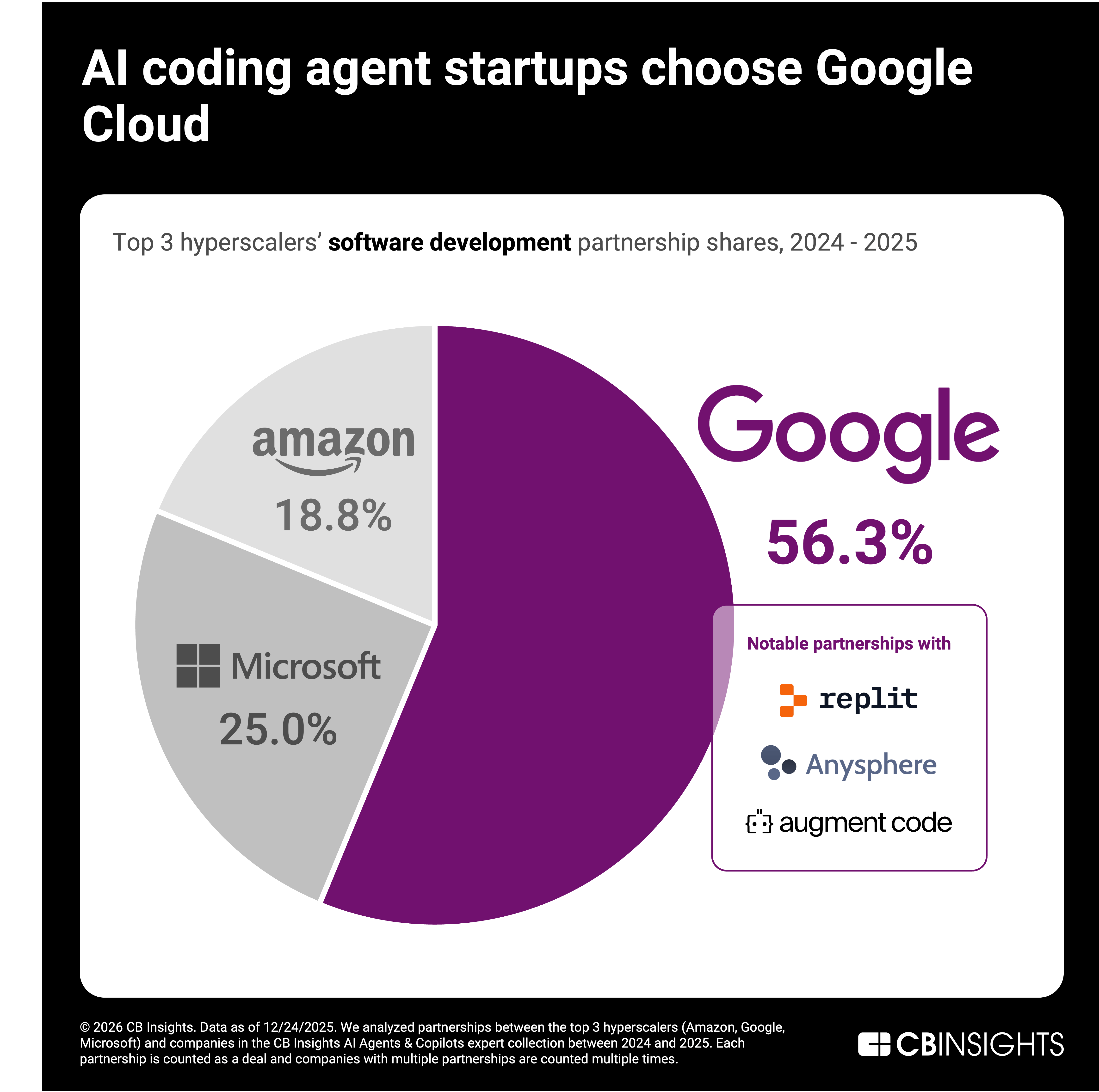

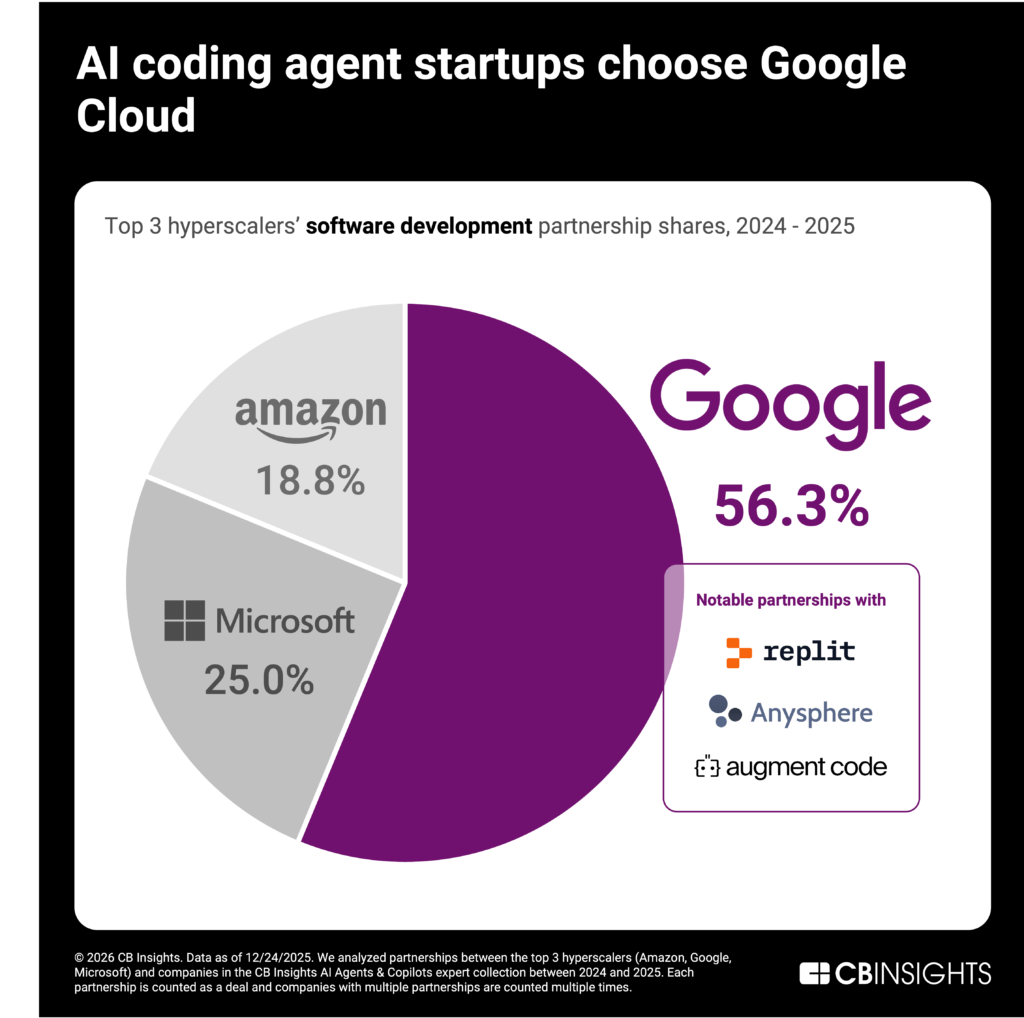

- Google (The Developer’s Choice): With a 57% share of software development partnerships, Google has become the de facto home for AI coding agents. By prioritizing developer-first workflows and open-source credibility, Google has effectively bypassed traditional enterprise procurement channels.

- Amazon (The Infrastructure Powerhouse): Commanding 64% of the customer service AI sector, AWS has turned its massive real-time data processing capabilities into a moat. By integrating with the Amazon Connect ecosystem, they are positioning themselves as the backbone of autonomous voice and chat resolution.

- Microsoft (The Compliance King): In highly regulated sectors like legal and healthcare, Microsoft holds a staggering 77% share of partnership activity. Their strategy revolves around "distribution-as-a-service," pulling AI-native startups into the existing Microsoft 365/Copilot flywheel.

Chronology of the Cloud-AI Shift

The evolution of these partnerships reflects the rapid maturation of the AI stack over the last two years:

2023: The Foundation Year

The early months of 2023 were defined by "compute-at-all-costs." Startups were largely agnostic, focusing on where they could secure GPU availability. However, as the focus shifted from simple chat interfaces to autonomous agents capable of executing tasks, the need for deep integration with cloud services became paramount.

2024: The Specialization Phase

By early 2024, the hyperscalers began to play to their historic strengths. Microsoft began aggressively targeting ISVs (Independent Software Vendors) in the legal and health sectors, offering them "compliance as a feature." Simultaneously, Google pivoted toward the developer community, recognizing that if they could win the "coding agent" war, they would control the underlying infrastructure of the next decade of software.

2025-2026: The Era of Vertical Integration

We are currently in the phase of "deep lock-in." Startups that were once small integrations are now becoming critical components of the hyperscalers’ product suites. For instance, the multi-million dollar commitments from startups like Harvey (legal) to Azure represent a permanent shift in how enterprise software is purchased and deployed.

Supporting Data: Why the Clusters Matter

The clustering of these partnerships provides a predictive map of future enterprise spending.

Coding: The "Bottom-Up" Strategy

Google’s dominance in coding AI is a masterclass in bottom-up adoption. Companies like Anysphere ($1B ARR), Replit ($240M ARR), and Harness ($250M ARR) are driving a paradigm shift where engineers dictate the infrastructure stack. Because Google’s Gemini models and open-source integrations are viewed as "developer-friendly," they are effectively winning the "war for the developer."

Customer Service: The "Scale" Strategy

The customer service AI market reached $1.6B in 2025. The success of companies like Zendesk, Kore.ai, and Intercom—all crossing the $100M ARR threshold—underscores the transition from scripted bots to autonomous agents. Amazon’s 64% lead here is not accidental; it is rooted in the fact that real-time voice and chat agents require the low-latency infrastructure that only AWS can scale reliably.

Regulated Industries: The "Trust" Strategy

Microsoft’s 77% share in legal and healthcare is the ultimate defensive moat. In these sectors, the primary barrier to entry is not technical prowess but regulatory trust. When Microsoft integrates Rhythmx AI into Dragon Copilot—which handles over 13 million patient encounters—they are providing a "regulatory umbrella" that shields startups from the complexities of HIPAA and other compliance regimes.

Official Responses and Strategic Perspectives

While the hyperscalers rarely comment on specific partnership percentages, their public earnings calls and whitepapers provide clear signals of their intent.

- Google Cloud: Leadership has frequently emphasized "openness" and "choice" as their primary differentiators. By positioning Google Cloud as the most flexible environment for LLM training and deployment, they aim to attract startups that are wary of the "walled garden" approaches of their competitors.

- Amazon (AWS): Amazon continues to highlight its "end-to-end" capabilities. Their messaging focuses on the reliability of the Amazon Connect ecosystem, arguing that when agents move from "chatting" to "doing" (e.g., executing a transaction via voice), infrastructure stability is the only metric that matters.

- Microsoft: Satya Nadella and his executive team have doubled down on the "Copilot" ecosystem. Their narrative is one of "distribution." Microsoft argues that a startup with a great product can achieve 10x growth by simply plugging into the Microsoft enterprise base, effectively trading autonomy for massive scale.

Implications: What This Means for the Future

The bifurcation of the AI agent market carries profound implications for the startup ecosystem, venture capital, and enterprise CIOs.

For Startups: The Death of Agnostic Development

The days of building "cloud-agnostic" AI agents are effectively over. Because of the depth of integration required—from compliance mapping in Azure to real-time voice processing in AWS—startups must now choose their "hyperscaler soulmate" early. The decision to partner with one provider now acts as a strategic lock-in that influences the startup’s GTM (Go-to-Market) strategy and technical roadmap.

For Enterprise CIOs: The Risk of Siloed Intelligence

As hyperscalers capture different verticals, CIOs are at risk of creating "intelligence silos." If the legal team is fully integrated into Microsoft’s ecosystem, while the development team is entrenched in Google, and the customer service department relies on AWS, the ability to create a unified data strategy for the enterprise becomes exponentially more difficult. CIOs will need to prioritize interoperability layers to prevent being held hostage by a single cloud provider’s roadmap.

The Long-Term Competitive Landscape

The market is shifting from "AI as a tool" to "AI as the operating system." The hyperscalers are no longer just selling compute and storage; they are selling the "intelligence layer" of the corporation. As these partnerships mature, we should expect to see fewer independent AI startups and more "acqui-hires" or deep-exclusive partnerships that turn these agents into core features of the hyperscalers’ own products.

The winners of this battle will not be the companies with the smartest models alone, but the companies that successfully integrated those models into the day-to-day workflows of the enterprise. By carving up the market into developers, customer service, and regulated industries, Google, Amazon, and Microsoft have set the stage for a decade of competitive friction that will define the modern digital economy.