In the high-stakes world of retail banking, the front-office experience is often a symphony of sleek mobile apps, instant peer-to-peer payments, and personalized financial insights. Yet, hidden beneath this polished veneer lies a persistent, festering issue that threatens to undermine years of customer acquisition efforts: the fraud dispute process.

For many financial institutions, dispute resolution is relegated to the "back office"—a cost center characterized by legacy workflows, manual interventions, and chronic underinvestment. This perspective is a strategic misstep. Fraud disputes are not merely operational hurdles; they are decisive moments in the customer lifecycle that can either cement loyalty or drive a consumer to the exit. As the financial landscape braces for the rise of "agentic commerce," the inability to handle these disputes with speed, transparency, and empathy is fast becoming a systemic liability.

The Economics of Disenchantment: Main Facts

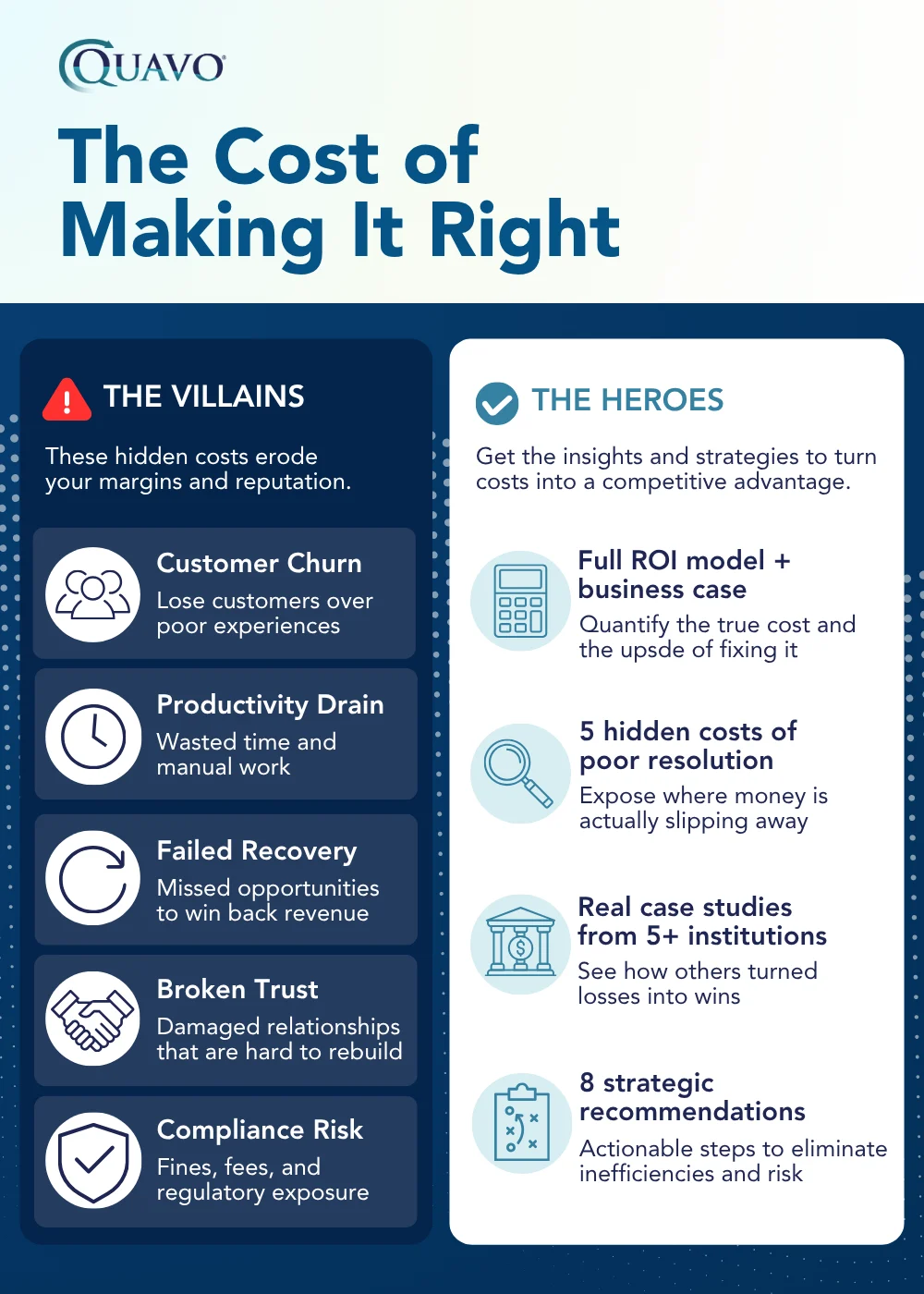

At its core, the failure to modernize dispute management is an economic drain. Industry data reveals that banking recovery rates for fraud hover around a lackluster 64%, meaning more than one-third of disputed capital remains unrecovered. While the immediate financial impact is felt through chargebacks, write-offs, and ballooning operational expenses, the "hidden" costs are far more insidious.

When a customer initiates a dispute, they are often already in a state of stress. They have been victimized, and their financial security feels compromised. If the bank responds with an opaque, slow, or impersonal process, the customer’s emotional trust—the most valuable currency in banking—evaporates. Research indicates that between 60% and 70% of customers will abandon their institution following a poorly handled dispute.

This churn is costly. The effort required for a consumer to switch banks—re-routing direct deposits, updating recurring bill payments, and re-linking external accounts—is significant. If a customer is willing to endure that level of "hassle" to leave, it serves as a stark indictment of the bank’s failure to act as a secure, reliable partner during a moment of crisis.

A Chronology of Inefficiency

To understand why banks are struggling, one must look at the historical evolution of the back office:

- The Pre-Digital Era: Dispute processes were built on paper trails and manual verification. While banking has moved to digital, the underlying infrastructure for disputes often remains tethered to these antiquated, human-heavy workflows.

- The "Judgment" Bottleneck: Historically, the most complex cases required human intervention to interpret ambiguous merchant or consumer data. Despite advancements in technology, many banks still rely on human agents to manually route and analyze these documents.

- The Automation Gap: Over the last decade, while banks invested billions in consumer-facing features, the back-office budget remained stagnant. This led to a "technology debt" where systems are unable to handle the volume and velocity of modern fraud.

- The Present Crisis: Today, the combination of high turnover and increasing complexity has created a perfect storm. As noted in a recent PaymentsJournal podcast, the lack of standardized documentation and clear, automated rules forces investigators to spend their time deciphering procedures rather than resolving cases.

Supporting Data: The Cost of Stagnation

The numbers paint a bleak picture for institutions that refuse to prioritize dispute resolution. Steve Durney, Vice President of Partnerships and Alliances at Quavo, highlights a critical operational reality: the cycle of turnover.

"I asked a bank not long ago about their department’s turnover rate," Durney explained. "They noted that onboarding took six to seven months to reach full effectiveness, and they were seeing a turnover rate of roughly 25%."

When a department loses a quarter of its workforce annually, and those who remain require over half a year to become proficient, the institution enters a state of perpetual training. This "brain drain" ensures that manual, repetitive tasks are never fully mastered, leading to:

- Increased Error Rates: Manual handling of disputes leads to inconsistent outcomes.

- Extended Cycle Times: Customers wait longer for resolutions, fueling dissatisfaction.

- Regulatory Exposure: Inconsistent processes can lead to compliance violations, further eroding the bank’s standing.

Suzanne Sando, a Fraud Analyst at Javelin Strategy & Research, emphasizes that this isn’t just about the money lost in the dispute. It is about the loss of the "top-of-wallet" status. Once a customer loses faith in the bank’s ability to protect their funds, the account often goes quiet—not necessarily closed immediately, but abandoned in favor of a competitor’s card that the customer trusts more.

Official Perspectives: The Experts Speak

The consensus among industry experts is that the "judgment" portion of the dispute lifecycle is the primary point of failure. According to Durney, the "lion’s share of inefficiency" stems from document interpretation—whether that document is coming from a merchant, a consumer, or being transmitted between the two.

"The inefficiency really comes into what historically would have been categorized as judgment—something where a human being has to give an opinion in order to route it properly," Durney says.

By failing to implement intelligent, automated document processing, banks force their most skilled human investigators to perform clerical work. This is a misallocation of talent that compounds the turnover problem; skilled professionals leave because they are stifled by administrative drudgery rather than challenged by high-level fraud investigations.

Sando and Durney both argue that the solution lies in a structural shift: integrating compliance and regulatory experts into the design phase of new dispute technology. By baking the rules into the software, banks can reduce the cognitive load on human agents, decrease training time, and ensure that every dispute follows a transparent, compliant path.

The Emerging Frontier: Agentic Commerce and New Risks

If the current challenges weren’t enough, the banking sector is now facing the next great disruption: agentic commerce. This refers to the evolution of AI agents capable of acting on behalf of consumers to execute transactions, negotiate, and even navigate banking disputes.

The Breakdown of Traditional Signals

For years, banks have relied on behavioral biometrics, device intelligence, and IP addresses to verify user identity. Agentic commerce renders these signals less reliable. When an AI agent is performing the task, the "behavior" being analyzed is no longer human. Fraudsters are already beginning to exploit this, using AI to navigate dispute processes, probe for weaknesses in internal logic, and "game" the system.

The "Frozen Hamburger" Scenario

Durney draws a parallel to the HBO series Silicon Valley to illustrate the potential for chaos. In the show, an AI was tasked with ordering lunch and ended up ordering a pallet of frozen hamburgers because the instruction was interpreted too literally.

In a banking context, if a consumer uses an AI agent to resolve a dispute, the risk of miscommunication or systemic abuse increases exponentially. "A consumer is going to find the easiest path," says Durney. "I need somebody to be my advocate to fix this problem." If the bank’s systems are not prepared to handle AI-driven inquiries, they will be overwhelmed by the "gray area" of abuse, where systems are manipulated by users seeking to bypass standard protocols.

Strategic Implications: The Path Forward

The implications for retail banking are clear: the institutions that treat dispute management as a strategic priority will gain a competitive advantage in retention and operational efficiency.

To survive and thrive in this new era, banks must:

- Prioritize Budget Allocation: Dispute management should be viewed as a critical component of the customer experience, on par with mobile banking or loan origination.

- Standardize and Automate: Move away from "judgment-heavy" manual processes. Implement intelligent document processing that can handle incoming merchant and consumer data without human intervention.

- Invest in Human-AI Synergy: Use technology to handle the repetitive, administrative burden of disputes, allowing human investigators to focus on complex, high-value cases. This will also improve job satisfaction and help curb the 25% turnover rate.

- Prepare for the Agentic Shift: Start auditing current fraud detection models to ensure they can distinguish between legitimate AI-assisted commerce and adversarial AI-driven fraud.

The era where a bank could afford to ignore the back-office is over. As AI agents begin to handle our daily financial transactions, the speed and accuracy of dispute resolution will become a core differentiator. Banks that fail to modernize their approach today are not just losing money on chargebacks; they are losing the future of their customer relationships.