In the competitive landscape of modern e-commerce, the difference between a completed sale and an abandoned cart often boils down to a single, critical decision at the final step of the customer journey: the payment method. As digital storefronts evolve, "Buy Now, Pay Later" (BNPL) services—such as Affirm, Afterpay, and Klarna—have transitioned from niche financial novelties to essential infrastructure for high-performing online retailers.

For merchants operating on platforms like WooCommerce, the question is no longer whether BNPL is "worth it," but rather how to strategically implement these tools to maximize Average Order Value (AOV) and conversion rates. With seamless integrations now available, the barrier to entry has never been lower.

The Economics of Frictionless Spending

At its core, the BNPL model addresses a fundamental psychological hurdle in retail: the "pain of paying." Most consumers are significantly more comfortable committing to four smaller payments of $70 than a single lump-sum payment of $280, even though the total financial outlay remains identical. By breaking down the barrier to purchase, BNPL services effectively normalize higher price points for the average consumer.

The data supports this psychological phenomenon. Merchants utilizing Afterpay have reported an average 22% lift in cart conversions and an impressive 40% increase in order values. Meanwhile, Affirm has seen its partners experience as much as a 70% boost in cart size. For merchants with an AOV exceeding $100, integrating BNPL is not just an added convenience; it is a powerful revenue-optimization engine.

Chronology of the BNPL Surge

The rise of BNPL was accelerated by the global digital transformation of the retail sector, but its roots lie in the shifting credit preferences of younger generations.

- Pre-2015: Traditional credit cards dominated, often tethered to high-interest revolving debt models that many younger consumers grew to distrust.

- 2015–2020: The emergence of specialized fintech firms—Afterpay, Affirm, and Klarna—began to reshape the checkout experience. These services offered transparent, installment-based lending that felt more like a budgeting tool than a credit card debt trap.

- 2020–2022: The pandemic served as a massive catalyst. As physical retail stalled and online shopping became the primary mode of commerce, BNPL adoption skyrocketed, moving from "nice to have" to a standard expectation for online shoppers.

- 2023–Present: The industry has entered a phase of consolidation and deeper integration. Platforms like WooCommerce have moved to simplify the deployment of these tools, effectively democratizing access to enterprise-grade payment technology for small and medium-sized businesses.

How the Mechanics Benefit the Merchant

One of the most persistent myths surrounding BNPL is that the merchant takes on the credit risk. In reality, the financial model is remarkably merchant-friendly.

When a customer selects a BNPL option, the merchant is paid in full immediately, just as they would be with a standard credit card transaction. The BNPL provider assumes the entirety of the fraud risk, manages all chargebacks and disputes, and takes on the burden of collections should a customer miss a payment.

For smaller purchases, this typically involves four interest-free installments paid over six weeks. For larger, high-ticket items, consumers can access monthly financing plans extending up to 36 months. By removing the financial risk from the merchant and placing it on the provider, BNPL acts as a de-risking mechanism for growing stores.

Choosing the Right Partner: Affirm, Afterpay, or Klarna

While running multiple BNPL providers is a viable strategy for some, many merchants prefer to pick one primary partner to simplify their accounting and customer messaging. Here is how the leading providers currently stack up:

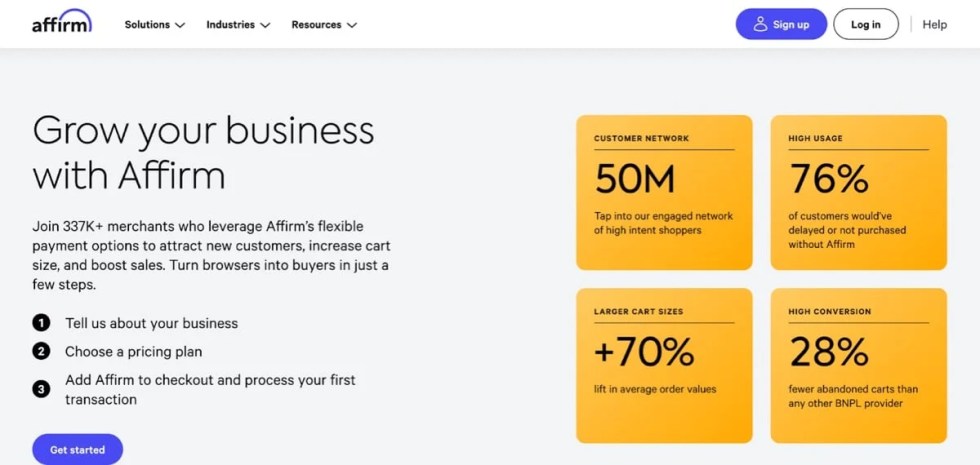

Affirm: The High-Ticket Specialist

Affirm is widely considered the gold standard for high-value purchases. With its ability to facilitate loans for items ranging from $35 to $30,000 and offer installment plans up to 36 months, it is the natural choice for retailers selling furniture, luxury electronics, or fitness equipment. A major differentiator for Affirm is its commitment to transparency—the company has built its brand on the absence of hidden fees, which helps build significant consumer trust during the checkout process.

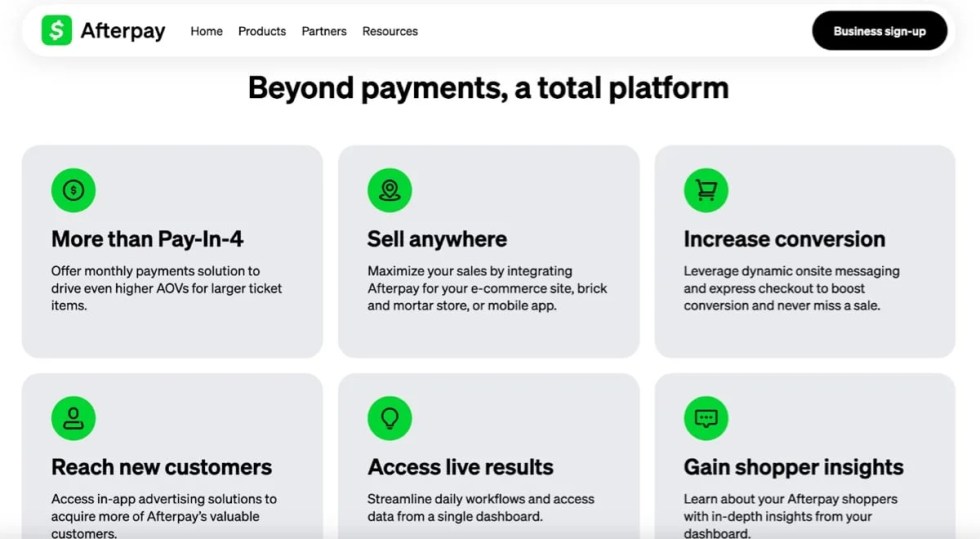

Afterpay: The Customer Acquisition Engine

Afterpay shines as a tool for customer acquisition. With over 57 million active users, the platform acts as a discovery engine for merchants. Studies indicate that approximately 30% of Afterpay shoppers are entirely new to the merchant they are purchasing from. Because its user base skews younger, Afterpay is the ideal partner for brands in the fashion, beauty, and lifestyle sectors. Its "Pay in 4" model is perfectly optimized for carts up to $3,000.

Klarna: The Global Powerhouse

For merchants with an international footprint, Klarna is the undisputed leader. Operating in 26 markets, it offers a level of global coverage that its competitors struggle to match. As a fully licensed bank, Klarna provides a robust, all-in-one payment ecosystem. Beyond just processing payments, Klarna provides marketing placements that surface the merchant’s products within the Klarna network, offering an additional layer of visibility for brands looking to expand their reach.

The Technical Implementation: A Two-Minute Process

The technical barriers to BNPL adoption have been effectively dismantled. For WooCommerce users, the process is streamlined:

- For WooPayments Users: Navigate to Payments → Settings → Payment methods. From there, you can toggle on Affirm, Afterpay, or Klarna. Once activated, the system automatically surfaces the relevant BNPL options to eligible customers at checkout.

- For Stripe Users: The process is mirrored within the extension settings under the "Payment methods" tab, where Stripe dynamically surfaces providers based on your region.

- For Other Gateways: If you are not currently using WooPayments or Stripe, you can install individual standalone extensions from the WooCommerce Marketplace. However, consolidating your payment infrastructure via WooPayments is highly recommended for the unified management of orders, refunds, and disputes.

Implications for Future Growth

The inclusion of BNPL is arguably the most cost-effective conversion optimization strategy available to modern retailers. However, the most successful merchants understand that these tools should not be hidden away.

Strategic implementation involves placing on-site messaging widgets on product and cart pages. By informing a customer early in the journey that they can purchase a $280 item for "4 payments of $70," you remove the mental friction that causes cart abandonment. These widgets are simple to install—often requiring only a one-line code snippet—and represent a significant opportunity to influence buyer behavior before they even reach the checkout page.

Critical Considerations

Before deploying these services, merchants must consider a few key constraints:

- Product Type: BNPL is designed for one-off retail transactions. If your store relies on recurring billing or complex subscription models, it is essential to verify compatibility with the provider first.

- Eligibility Thresholds: Every provider sets its own minimums and maximums based on local regulations. Very low-value items or extremely high-value B2B orders may not always qualify for these programs.

- Geographic Alignment: Always audit your traffic data. If your primary customer base resides in a region not supported by your chosen provider, the conversion lift will be negligible.

Conclusion

The shift toward BNPL is a fundamental evolution in how we conduct commerce. By lowering the barrier to entry for shoppers and providing a seamless, risk-free financial bridge, merchants can drive higher conversion rates and larger order sizes.

For the average WooCommerce store owner, the setup time is measured in minutes, yet the long-term impact on the bottom line is measured in thousands of dollars of recovered revenue. In an era where customer attention is fleeting and cart abandonment remains a persistent challenge, providing flexible payment options is no longer just a trend—it is a core requirement for any merchant looking to compete in the global marketplace.