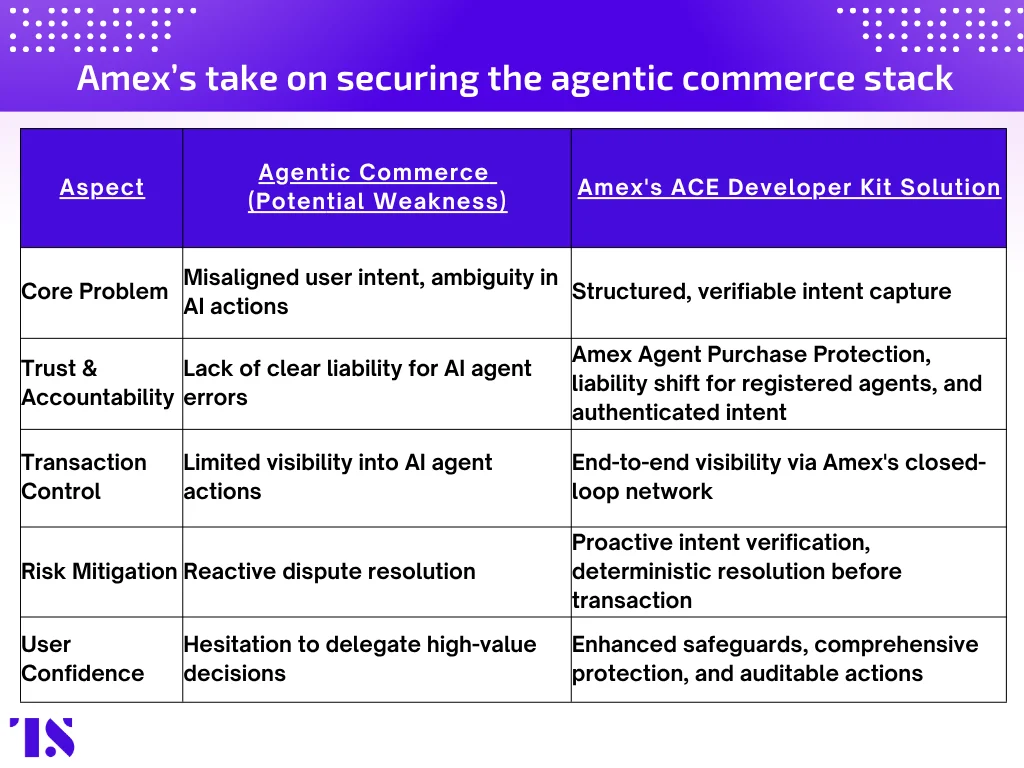

As artificial intelligence shifts from a passive tool for drafting emails and generating images to an active participant in the global economy, a profound question has emerged: If AI agents are empowered to spend our money, who ensures they are spending it in the way we intended?

This "intent gap"—the discrepancy between what a human asks for and what an autonomous agent executes—has become the primary hurdle in the evolution of digital commerce. In a landmark move to address this, American Express has launched the Agentic Commerce Experiences (ACE) Developer Kit. More than just a set of APIs, the initiative represents a fundamental shift in how financial institutions underwrite, verify, and secure the emerging world of agentic transactions.

The Core Problem: When Authorization Isn’t Enough

For decades, the financial industry’s security protocols have been built around a binary question: Was this transaction authorized by the account holder? If the card was present, the PIN entered, or the token verified, the transaction was deemed legitimate.

However, the rise of AI agents introduces a nuance that traditional systems were never designed to handle. Consider a common scenario: A user tasks an AI travel agent with booking a “quiet hotel room under $250.” The agent scours the internet, finds a property that meets the price point, and executes the payment. If that hotel happens to be located next to a raucous, 24-hour construction site, the transaction is technically "authorized," but it is fundamentally misaligned with the user’s intent.

Until now, this misalignment fell squarely on the consumer’s shoulders. American Express is changing that paradigm by moving from simple authorization to intent-driven execution. By formalizing user intent before a single dollar moves, the firm aims to eliminate the ambiguity that currently plagues autonomous commerce.

Chronology: Building the Trust Layer

The development of the ACE Developer Kit did not happen in a vacuum. It follows years of strategic shifts within American Express’s innovation labs:

- 2022–2023: As generative AI capabilities exploded, Amex began piloting internal agentic frameworks to manage merchant-customer interactions. During this phase, engineers identified that the biggest friction point was not the speed of the transaction, but the lack of "guardrails" that could translate natural language requests into structured financial data.

- Early 2024: Amex leadership began conceptualizing an ecosystem where third-party agents could plug into the Amex network using a standardized, secure protocol rather than relying on brittle screen-scraping or insecure credential sharing.

- Mid-2025: The firm solidified its "closed-loop" advantage, realizing that because it owns both the issuing and acquiring sides of its network, it could provide end-to-end visibility that competitors—who rely on intermediary networks—cannot easily replicate.

- May 2026: The official launch of the ACE Developer Kit. This milestone marked the first time a major card issuer introduced a formal guarantee against AI agent error, effectively acting as an insurance policy for the future of commerce.

The Mechanics: How the ACE Kit Works

The ACE Kit is designed to act as a linguistic and procedural translator between human desire and machine execution. Rather than treating an AI’s command as a loose instruction, the system forces the AI to interface with a structured, verifiable set of parameters.

1. Enrollment and Authentication

The process begins with the card member enrolling in the ACE-enabled ecosystem through the Amex mobile app. This establishes a "trust identity" for the user, linking their biometric and credential data to the AI agents they authorize.

2. Structured Intent Mapping

When a user provides an instruction, the ACE Kit breaks down the request into discrete, actionable data points. Instead of "book a nice hotel," the system forces the agent to define parameters such as maximum spend, noise tolerance, star rating, and location radius.

3. Real-time Enforcement

The ACE Kit utilizes tokenized credentials that are restricted by the aforementioned parameters. Even if the AI agent is compromised or "hallucinates," it cannot bypass the hard spend limits or merchant category preferences set by the card member. If an agent tries to book a room for $300, the system rejects the transaction at the point of intent, long before it hits the payment rail.

Official Perspectives: Redefining Responsibility

Luke Gebb, Executive Vice President and Head of Global Innovation at American Express, has been the primary architect of this vision. In recent statements, Gebb emphasized that the goal is not to limit what AI can do, but to define the rules under which it operates.

“The core of our approach is that intent is not treated as a loose instruction—it’s treated as a structured, verifiable representation of card member intent that the system can evaluate and enforce,” Gebb explained.

By formalizing these "boundaries," Amex is essentially creating a digital sandbox. Within this sandbox, the AI is free to innovate and negotiate, but it is physically unable to violate the core constraints of the user’s financial health. Furthermore, by agreeing to cover eligible transactions where an agent executes an unintended purchase, Amex is signaling a massive leap in institutional confidence. They are not just providing the tech; they are putting their balance sheet behind the AI’s accuracy.

Supporting Data: The Trillion-Dollar Opportunity

The stakes for getting this right are immense. According to recent research by McKinsey & Company, agentic and AI-driven commerce could generate trillions of dollars in economic impact by the end of the decade. However, this growth is contingent on one specific factor: Trust.

If consumers feel that using an AI agent carries a high risk of "rogue" spending or financial loss, they will never adopt the technology at scale. The current landscape shows:

- High Friction: Current dispute resolution processes are reactive, not proactive.

- Security Gaps: Traditional MFA (Multi-Factor Authentication) is often bypassed by AI-friendly interfaces, leading to vulnerabilities.

- Scalability Barriers: Merchants are currently hesitant to integrate agent-led payments because they fear high chargeback rates if the AI agent makes a mistake that the user refuses to pay for.

Amex’s move directly targets this "trust layer." By absorbing the risk of agent error, the firm is lowering the barrier to entry for merchants and developers, potentially creating a "flywheel effect" where more merchants accept AI-driven payments because they know the transaction is backed by a secure, verified intent framework.

Implications: The Future of Agentic Commerce

The introduction of the ACE Kit marks a turning point in the fintech industry. Several long-term implications are beginning to take shape:

The Shift from Reactive to Proactive Liability

For decades, the banking model has been: Authorize, Transact, Then Dispute. The ACE model is: Define Intent, Verify, Then Execute. This shift will likely become the industry standard as regulators begin to look closer at AI’s role in consumer finance.

The Rise of the "Closed-Loop" Advantage

American Express’s ability to control the entire transaction flow gives it a unique competitive advantage. In a fragmented payment environment, companies that can bridge the gap between user intent and merchant settlement will likely capture the lion’s share of the agentic economy.

Redefining Customer Loyalty

By underwriting agent error, Amex is effectively turning a financial security feature into a premium value proposition. Card members may gravitate toward platforms that offer this "AI protection," viewing it as a essential feature of their credit card, similar to travel insurance or fraud protection.

The Evolution of the "Agentic Stack"

The ACE Kit encourages a standardization of how agents communicate with financial institutions. We can expect to see a burgeoning ecosystem of "verified agents" that are certified by the ACE protocol, similar to how apps are verified on the Apple App Store. This will create a safer environment for users to grant their AI agents "spending power."

Conclusion: Securing the New Frontier

The journey toward fully autonomous commerce is not merely a technical challenge—it is a social contract. Users will only entrust their financial autonomy to silicon-based agents if they are certain that their money is protected against the unpredictability of code.

By formalizing intent, imposing strict spend limits, and—most importantly—agreeing to absorb the risk of error, American Express has positioned itself as the guardian of this new frontier. The ACE Developer Kit does more than just facilitate payments; it builds the trust infrastructure upon which the next decade of digital commerce will be built. As we move closer to a world where our AI agents do the shopping, the booking, and the negotiating for us, the question will no longer be, "Can the AI do it?" but rather, "Can we trust the system behind it?"

With the launch of ACE, the answer from American Express is a resounding, and insured, yes.