Executive Summary: The Shifting Financial Landscape

This week’s market activity reveals a profound maturation point for the financial services industry. As we analyze the closing prices through Thursday, a clear pattern emerges: the binary opposition between "nimble fintech" and "incumbent banking" is rapidly dissolving. We are witnessing an era of convergence where consumer expectations for digital-first experiences are colliding with the institutional requirements of trust, regulatory compliance, and long-term retention.

This report tracks these strategic pivots, examining how companies like Chime, Robinhood, Intuit, American Express, and JPMorgan Chase are maneuvering to capture market share. By moving beyond simple growth-at-all-costs models, these entities are signaling a transition toward integrated, high-utility financial ecosystems.

Chronology of Market Developments

1. Chime (CHYM): The Institutional Pivot

- Close: $19.28

- The Narrative: Chime’s recent performance reflects its evolution from a venture-backed disruptor into a full-stack financial institution. Having largely conquered the entry-level digital banking space, the company is now pivoting toward sophisticated monetization and product depth.

- Implications: As Chime matures, it faces the "incumbent’s paradox." By deepening product exposure, the firm inherits the systemic scrutiny traditionally reserved for legacy banks. Trust, cybersecurity, and responsible growth are no longer just PR talking points; they are now the primary KPIs that dictate market valuation. Investors are beginning to price Chime not on user acquisition volume, but on the lifetime value (LTV) and stability of its user base.

2. Robinhood (HOOD): Democratizing the Private Markets

- Close: $76.31

- The Narrative: Robinhood is aggressively targeting the structural divide between public and private wealth creation. By offering retail investors access to pre-IPO assets—historically the exclusive domain of venture capital and institutional private equity—the platform is attempting to redefine the retail trading value proposition.

- Implications: This move is a double-edged sword. While it expands the investment universe for the average consumer, it introduces significant complexity regarding liquidity and risk management. If Robinhood successfully bridges this gap, it secures a massive competitive moat; if it stumbles, it risks regulatory pushback and potential losses for a demographic that may lack the risk tolerance required for private market volatility.

3. Intuit (INTU): The SMB Operating System

- Close: $407.97

- The Narrative: Intuit’s strategy remains focused on dominating the small-to-medium business (SMB) stack. By integrating labor and workforce management into its QuickBooks ecosystem, Intuit is positioning itself as the central "operating system" for businesses, moving beyond mere accounting.

- Implications: The underlying thesis here is that AI will collapse fragmented software stacks. Instead of businesses using five different tools for payroll, tax, HR, and payments, Intuit aims to consolidate these into a singular, AI-driven decision engine. The success of this move will determine whether Intuit remains a software vendor or evolves into an automated business partner that influences operational decision-making.

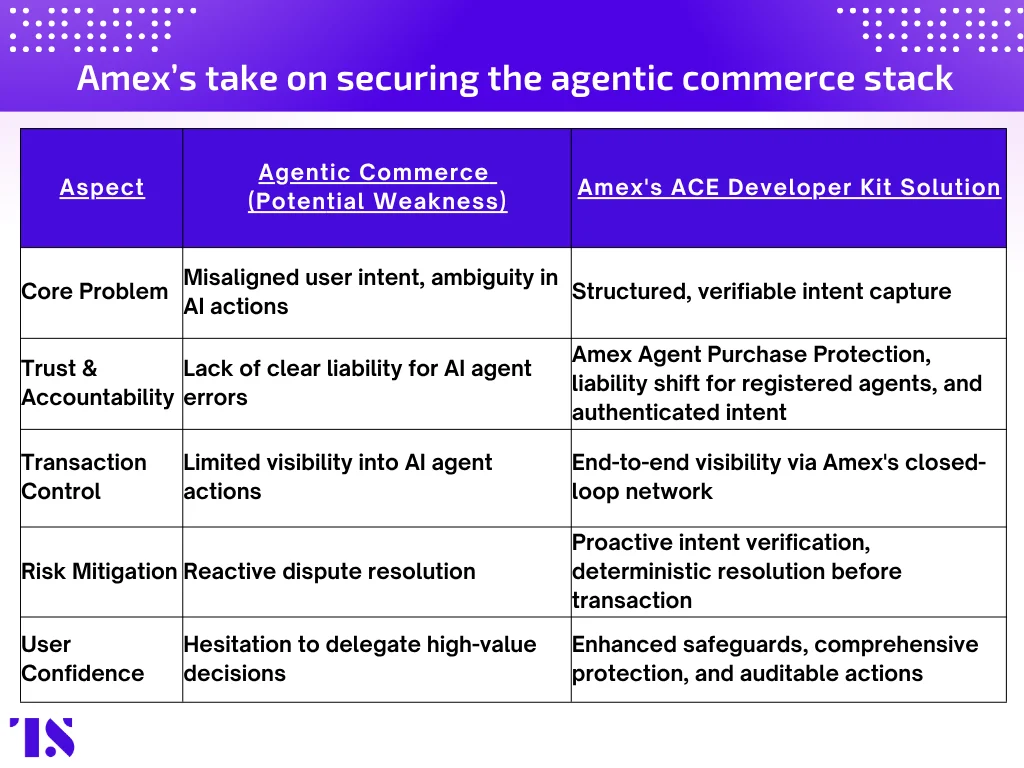

4. American Express (AXP): The Workforce Enablement Play

- Close: $317.40

- The Narrative: While many firms treat AI as a back-end technology upgrade, American Express is framing it as a front-line workforce requirement. Their strategy focuses on upskilling SMB clients to ensure they can leverage AI tools effectively.

- Implications: This is a brilliant defensive play. By positioning itself as an educator and enabler, Amex ensures that its financial products remain embedded in the business growth cycle. It’s no longer just about providing credit or processing payments; it’s about ensuring the client’s success, thereby deepening the relationship and reducing churn.

5. JPMorgan Chase (JPM): The Hybrid Model

- Close: $307.50

- The Narrative: Chase continues to challenge the narrative that digital-only is the future. Instead, they are doubling down on a hybrid strategy, utilizing their vast physical branch network as a competitive advantage to provide guidance for complex financial life events.

- Implications: Gen Z’s preference for hybrid banking is forcing a convergence. While fintechs are seeking ways to establish trust through "offline" credibility, Chase is refining its UX to match the agility of digital challengers. The result is a middle ground where the winner is whoever offers the best blend of modern digital convenience and personalized, human-centric support.

Supporting Data and Market Analysis

The market’s reaction to these developments suggests that investors are shifting their focus away from growth metrics that don’t translate to the bottom line.

- Valuation Multiples: Companies demonstrating clear pathways to multi-product integration (Intuit, Amex) are seeing more resilient trading ranges compared to those still heavily reliant on single-product acquisition models.

- Consumer Sentiment: Data indicates a growing demand for "financial safety" in the face of macro-economic uncertainty. This favors established players like Chase and maturing fintechs like Chime that have begun to mirror bank-like security features.

- The AI Premium: The market is currently applying a valuation premium to companies that can demonstrate tangible productivity gains for their end-users—specifically those using AI to automate workflows rather than just generate content.

Official Responses and Strategic Outlook

While official quarterly guidance varies, the tone across the industry is one of measured expansion.

- Institutional View: Representatives from the major banks note that the "fintech threat" has evolved into a "fintech partnership" opportunity. The focus has shifted from disruption to integration.

- Fintech Perspective: Leading fintech executives emphasize that "scale brings responsibility." The messaging from firms like Chime and Robinhood increasingly highlights compliance, stability, and long-term product roadmaps, signaling a departure from the "move fast and break things" mantra of the previous decade.

Implications for the Future of Finance

The End of "Digital vs. Physical"

The most critical takeaway from this week’s analysis is that the "digital versus physical" debate is effectively dead. The future of the industry is a "phygital" model. For fintechs, this means the need for trust-building, potentially through physical touchpoints or robust, bank-grade customer service. For incumbents, this means digital UX must be seamless, intuitive, and as responsive as any Silicon Valley app.

The Rise of the "Decision Engine"

We are entering the era of the "Financial Decision Engine." Software is moving from recording transactions to managing outcomes. Intuit and Amex are leading the charge here, moving toward platforms that tell business owners not just "what happened," but "what to do next." This transition will likely result in a new class of financial software that is far stickier than traditional tools, as it becomes deeply intertwined with the operational success of the enterprise.

Risk and Access

Robinhood’s push into private markets poses a long-term question for regulators and the industry: how much democratization is enough? The move suggests that the barriers between private equity and retail investors are becoming porous. If this trend holds, we could see a fundamental change in the composition of retail portfolios, which may necessitate new educational frameworks and protections to ensure that retail investors are equipped to manage the inherent risks of less liquid, private assets.

Final Thoughts for Investors

As we look toward the remainder of the fiscal year, investors should prioritize companies that exhibit:

- High-Utility Integration: Businesses that own the user’s workflow, not just the transaction.

- Institutional Maturity: Fintechs that have transitioned to a culture of compliance and long-term retention.

- Workforce Empowerment: Firms that provide tangible educational value to their customers, thereby ensuring their own longevity in the client’s ecosystem.

The market is no longer rewarding the disruptors for merely existing; it is rewarding those that can build sustainable, integrated, and trustworthy platforms for the next decade of commerce.

This analysis is part of Tearsheet PRO’s weekly 10-Q Newsletter. To stay ahead of the curve as strategy meets market reaction, subscribe to PRO for the full 10-Q story every Friday.