In the high-stakes world of corporate governance, three words carry more weight—and trigger more anxiety—than perhaps any others: “Voluntary and timely.” These terms serve as the bedrock of modern corporate resolution agreements with the Department of Justice (DOJ) and the Securities and Exchange Commission (SEC). They are the golden ticket to leniency, the difference between a declination and a nine-figure penalty. Yet, as a comprehensive analysis by Corporate Compliance Insights (CCI) reveals, this critical obligation remains one of the most consequential, yet least defined, requirements in the regulatory landscape.

For general counsels and chief compliance officers, the promise of “guaranteed” credit for self-disclosure is increasingly viewed as a high-stakes gamble. An analysis of nearly two dozen enforcement actions from the past decade paints a messy, inconsistent picture where the “timeliness clock” is often shrouded in mystery, leaving corporations to guess at a threshold that the government refuses to quantify.

The Myth of the "Clock"

The primary source of frustration for compliance practitioners is the absence of a standardized definition for “timeliness.” In the nine enforcement cases examined by CCI where companies successfully received credit for timely disclosure, only two provided a measurable time window. In one instance, a company reported within three months of identifying potential misconduct and mere hours after internal confirmation. In another, a board of directors notified regulators within two weeks of learning of the issue.

For the remaining seven cases, the language used by authorities is intentionally vague: “voluntarily and timely,” “promptly,” or “prompt, voluntary self-disclosure.” There is no objective clock, no defined threshold, and no guidance on when the race officially begins. Does the clock start when the first whistleblower tip hits the HR inbox? When the legal department opens a preliminary inquiry? Or the moment the company reaches internal confirmation of a violation?

The government’s message to those who get it right is a circular, unhelpful refrain: You were timely. The message to everyone else, however, is a harsh lesson in the dangers of delay.

A Chronology of Missed Opportunities and External Triggers

The enforcement record suggests that for many companies, the “timeliness” question is rendered moot long before they decide to pick up the phone. In several high-profile cases, the decision to disclose was overtaken by external events—whistleblowers, investigative journalists, or parallel government inquiries—that effectively slammed the door on the possibility of voluntary disclosure credit.

The External Trigger Pattern

- The Global Spirits Case: A former employee bypassed the company’s internal reporting structure, copying both American and Indian government authorities on correspondence regarding alleged misconduct. Because the government was alerted before the company came forward, the firm was denied voluntary disclosure credit, resulting in a $19.6 million penalty.

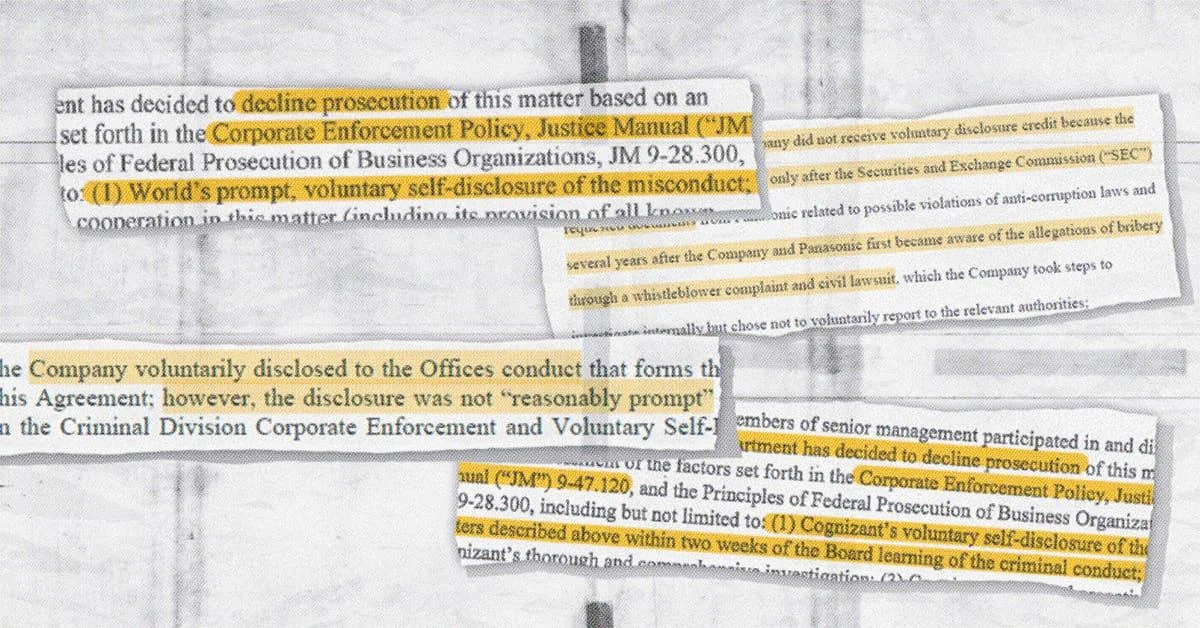

- The SAP SE Case (2024): In a deferred prosecution agreement (DPA) involving the German software giant, the company failed to receive credit for voluntary disclosure because investigative reports in South Africa had already made the allegations public. While SAP earned credit for immediate cooperation after the press reports appeared, the opportunity for VSD (Voluntary Self-Disclosure) credit was gone. The result was a staggering $119 million in criminal penalties and $103 million in disgorgement.

The Deliberate Delay

In contrast to cases where companies were beaten to the punch, other firms had the information in hand but chose to wait, often with devastating financial consequences.

- Panasonic Avionics: Upon receiving word of bribery allegations via a whistleblower and subsequent civil litigation, the company launched an internal investigation. Despite identifying the misconduct, the company opted against self-reporting. It was only after the SEC issued a document request that the company finally engaged with the regulators. The cost of this delay? $137.4 million and the imposition of a two-year compliance monitor.

- Albemarle: This case illustrates the danger of partial or delayed reporting. After confirming misconduct in one jurisdiction, the company waited more than nine months before disclosing. While they eventually reported related conduct in three additional countries, the delay on the original matter stripped them of full credit. The total financial impact reached approximately $196 million.

Supporting Data: The Cost of Waiting

The financial implications of missing the timeliness window are stark. In the cases analyzed by CCI, companies that failed to meet the government’s nebulous standard for timeliness faced criminal penalties and disgorgement averaging between $140 million and $170 million.

These figures underscore the “Venn diagram” nature of compliance: what a company deems a reasonable amount of time to conduct a thorough investigation often conflicts with the government’s desire for immediate, raw intelligence. The industry is trapped in a tension between the need to "get it right" before reporting and the pressure to report before the authorities find out from someone else.

The "Contamination" of Credit

The experience of Walmart serves as a cautionary tale for multinational corporations. The retailer proactively disclosed misconduct in Brazil, China, and India—actions that, in isolation, would have garnered substantial voluntary disclosure credit. However, because the government was already investigating related conduct in Mexico, the entire narrative was tainted. The disclosure of one matter contaminated the potential for credit across the board, demonstrating that the DOJ views the compliance record not as a series of isolated events, but as a holistic assessment of corporate integrity.

Official Responses and Practitioner Perspectives

The difficulty of this environment cannot be overstated. Taryn McDonald, a partner at Haynes Boone, notes that the tension between thoroughness and speed is the defining challenge for modern compliance officers.

“[The DOJ wants] you to disclose all relevant facts, but they also want you to disclose very, very early,” McDonald told CCI. “That’s really hard to do. If you make a decision to disclose, you’re not waiting till it’s all tied up with a bow. It’s just not going to be possible.”

The DOJ’s stance, while theoretically aimed at incentivizing transparency, creates a paradox. If a company reports too early, they may provide incomplete or inaccurate information, which can jeopardize the investigation. If they report too late, they lose the benefits of self-disclosure. The lack of a "safe harbor" period or a clearly defined grace period leaves firms in a constant state of defensive maneuvering.

Strategic Implications: Building a Resilient Culture

Given the unpredictability of the enforcement landscape, what is a compliance officer to do? The consensus among legal experts is that the decision to disclose is rarely a simple mathematical calculation. It is a nuanced risk analysis that weighs the nature of the conduct, the prevalence of the issue, and the likelihood of discovery by third parties.

1. Prioritize Internal Culture

The first line of defense is not a reporting protocol, but a culture of integrity. As McDonald emphasizes, having a robust compliance program that encourages employees to report issues internally is the only way to ensure the company has the information necessary to make a disclosure decision in the first place. If an organization lacks the internal mechanisms to identify misconduct, it is effectively blind to its own liabilities.

2. Prepare for the "Trigger"

Companies must operate under the assumption that an external trigger—a disgruntled employee, a leak, or a news report—is always a possibility. This necessitates a "readiness posture" where the legal team has pre-vetted response protocols, ensuring that if a decision to disclose must be made, the company can move within days, not months.

3. Embrace the Reality of Risk

The enforcement record makes one thing clear: there is no way to eliminate the risk of a penalty entirely. However, the data suggests that companies that control the narrative—by disclosing as soon as the core facts are understood, rather than waiting for a finalized investigation—are consistently in a better position than those who are forced to disclose under the pressure of an external inquiry.

Conclusion

The DOJ’s “voluntary and timely” mandate remains a double-edged sword. While it offers a path to reduced penalties, it is a path paved with uncertainty. The enforcement record demonstrates that the government’s definitions are fluid, heavily dependent on the specific context of each case, and—most importantly—subject to the race against third-party disclosures. For the modern corporation, the lesson is clear: in the absence of a defined clock, speed is the only currency that matters. Those who hesitate, or who rely on their own internal timelines, often find that the government has already decided the clock has run out.